Waterhouse VC is a fund that specialises in global publicly listed and private businesses related to wagering and gaming sectors. The fund is only available to wholesale investors.

Since inception in August 2019, Waterhouse VC has achieved a gross total return of +3,775% (annualised at 83%), as at 31 August 2025, assuming the reinvestment of all distributions.

Land of the Rising Sums

In 1854, American Commodore Matthew Perry’s "Black Ships" forced open Japan’s ports, ushering in unequal treaties that drained gold, placed foreigners beyond Japanese law and threatened economic sovereignty. The 1868 Meiji Restoration was Japan's response: modernise institutions, adopt Western technology on Japanese terms, and reclaim control over their economic destiny.

Today, Japan's wagering market faces a similar challenge. Gambling has been banned for more than a century, with only tightly managed exceptions. Legalised betting on horse racing predates the war and after 1945, three further public sports were given carve-outs to fund reconstruction and local finance: horse racing dominates at ¥4.4 trillion (US$29.7 billion) in turnover; boat racing adds ¥2.5 trillion; keirin cycling ¥1.3 trillion; with motorcycle ("auto race") comprising the remainder. These state-sanctioned pari-mutuel sports generated ¥8.5 trillion (US$57 billion) in turnover in 2024.

Yet an estimated ¥6.4 trillion (US$45 billion) of bets were placed with online operators offering products Japan's century-old framework cannot match. Like gold flowing through Yokohama's treaty ports 170 years ago, this is a loss of control.

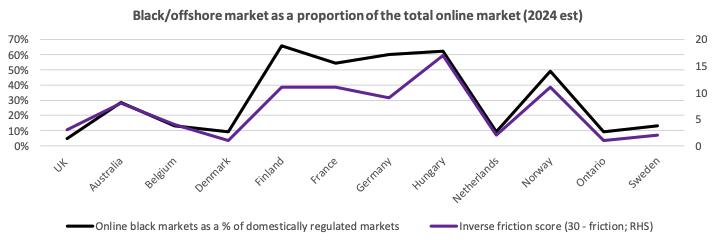

The harder it is to access regulated betting, the more players turn offshore. A warning for Japan. Source: Regulus Partners

This month we examine Japan's wagering paradox: how the world's third-largest economy became one of the world's largest sources of unregulated betting revenue, why generational change makes the status quo unsustainable, and where the opportunity lies for those positioned to help Japan modernise its wagering market.

Commodore Perry Coming Ashore at Yokohama, attributed to Wilhelm Heine. Source: Yokohama Archives of History

Monopoly Money

Japanese racing has become the global gold standard, with success stemming from a crucial advantage: monopoly power. Racing is able to capture betting turnover that would otherwise flow to sports betting or online gaming. Liquidity is propelled by scale and wealth: ~120 million people, high incomes, and few legal alternatives.

The Japan Racing Association (JRA) returns 75% of pools to winning bettors. Of the 25% deduction, 10% goes to the national treasury and the balance funds operations and prize money. The ¥4.4 trillion (US$29.7 billion) of horse-racing turnover (JRA + NAR) sustains world leading prize purses, draws deep, quality fields, and creates an engaging product.

While liquidity runs deep, Japan is hard for professional syndicates to access. Most avoid it because of the complexity. Those who do enter have two routes: bet in cash and manage repatriation, or establish a Japanese company with domestic banking and pay local tax. Pools are domestic only (no international commingling) and rebates aren’t offered. For the few willing to build that capability, it’s highly rewarding, particularly as there’s less sharp competition.

Japan’s four codes all grew in 2024. Keirin turnover rose 11%, boat racing 4.1% and motor racing 7.8%. There is clear intent from each sport to engage younger audiences but with such limited legal betting options it is unsurprising that the overall pie is growing.

Huge crowds at the Japan Cup. Source: CNN

Uma Musume. An anime-style game is bringing a new audience to racing. The game has raked in >US$2 billion in revenue since it launched in 2021. Source: Uma Musume

Pachinko to Plinko

Pachinko reveals the scale of the appetite beyond sport. This noisy pinball variant operates through a legal loophole that predates modern sweepstakes. Players combine skill and luck to win metal balls; Pachislot players use tokens on machines resembling physical slots. Both exchange winnings for prizes in-parlor, then swap prizes for cash at "unrelated" shops nearby.

¥15.7 trillion (US$110 billion) was wagered on these machines in 2023: ¥8.2 trillion pachinko, ¥7.5 trillion pachislot. Nearly double the legal sports market, yet technically, not gambling.

Pachinko parlor in Japan. Source: Waterhouse VC

The model is dying. From 18,000 parlors in the 1990s peak to under 8,000 today (Source: AGB). COVID accelerated the decline, but demographics and a thriving offshore market will seal it. Young players won't tolerate physical tokens when digital alternatives exist where users can bet with one-tap deposits, gain instant settlement, and have unlimited product choice. When the legal path requires three physical steps, players choose the single click.

Digital alternatives to Pachinko and Plinko. Source: Stake

Product Gap

Japan's sports passion runs far beyond the four pari-mutuel codes. Baseball is a national staple. J-League football fills stadiums. Sumo, volleyball, basketball, and rugby all have loyal followings. Yet outside the four codes and pachinko parlors, the only sanctioned option is Toto, officially called the Sports Promotion Lottery, which launched in 2001.

Toto offers various football pools, such as predicting match results for the main games each round, or goal totals for selected matches – all at ¥100 per ticket. By law, the prize pool cannot exceed 50% of sales, making the house edge a minimum 50% compared to racing's 25% take. There's also "BIG," where a computer randomly picks for you.

With payouts that would make a bookmaker blush and no ability to bet on individual matches or specific outcomes, Toto lacks any features that resemble a modern sportsbook.

Kiosk in Tokyo sells toto coupons. Source: Web Japan

Meiji Moment

In June 2025, the national legislature of Japan revised law to ban the launch and promotion of online casino services targeting Japan, enabling takedowns, pressure on payment intermediaries, and cooperation with overseas regulators. Tokyo has asked foreign licensing hubs to block Japan-based users, and removal requests are being sent to offshore sites, affiliates, and influencers. These steps raise friction but will not reverse behaviour without a competitive legal product.

Japan stands at its Meiji moment for gambling. When value leaked through treaty ports, Japan modernised. Today the leak is digital, and the answer is the same.

It is too soon to judge the crackdown, but Japan’s starting point is unlike mature markets. Online sites did not steal share. They built the market because there was no domestic alternative. Habits formed online are hard to unwind, and VPNs keep the path open. Enforcement can raise friction, but only competitive legal options will change behaviour.

Hong Kong offers a useful case study. The Hong Kong Jockey Club, the territory’s exclusive wagering outlet, handled US$41 billion in 2025, including a record US$22 billion from football (up 7.8% YoY), with basketball now approved to roll out next. Breadth of product grows the regulated market and keeps money onshore.

If Japan opens, control will come first. Expect a selective regime with few licences and high bars on KYC, local presence, payments, integrity, and advertising. The advantage will sit with groups that already own the fan relationship and can pair it with credible local partners and access to government.

Japan's offshore leakage dwarfs other markets, but the solutions are consistent. Waterhouse VC backs the infrastructure that makes regulated betting competitive: reducing friction while maintaining compliance.

Japan won't abandon control for revenue. When reform comes, it will demand infrastructure that delivers both - offshore convenience within Japanese standards. Those building that bridge today will own tomorrow's market.

Pitch Us

If you know any gambling tech companies seeking capital or distribution support, our new 'Pitch' page makes it simple to connect with our investment team.

Media

Tom joined Ausbiz to discuss the rapid rise of prediction markets, Flutter’s sudden exit from India due to new legislation, and how the UK Government’s strict gambling regulations are fueling the growth of black-market operators.

Waterhouse VC hosted a webinar with Brandt Page, CEO and founder of Bitblox Games. We discuss how Bitblox is innovating with unique, fast-paced crypto-based games, the huge market they are targeting, and their expansion plans.

For wholesale investors interested in following wagering and gaming industry news and trends, please follow our updates on Twitter (@waterhousevc) and WaterhouseVC.com.

DISCLAIMER AND IMPORTANT NOTES

Please note the above information in relation to Japan Racing Association, Stake, National Association of Racing, Yokohama Archives of History, CNN, Regulus Partners, The Hong Kong Jockey Club, Uma Musume is based on publicly available information and should not be considered nor construed as financial product advice. The information provided in this document is general information only and does not constitute investment or other advice. Readers should consult and rely on professional investment advice specific to their individual circumstances.

Not for Release or Distribution in the United States of America

This material may not be released or distributed in the United States. This material does not constitute an offer to sell, or a solicitation of an offer to buy, any securities in the United States or any other jurisdiction in which such an offer would be illegal. The units in the Fund have not been, and will not be, registered under the U.S. Securities Act of 1933, as amended (the U.S. Securities Act) or the securities laws of any state or other jurisdiction of the United States. Accordingly, the units in the Fund may not be offered or sold in the United States unless they are offered and sold, directly or indirectly, in transactions exempt from, or not subject to, the registration requirements of the U.S. Securities Act and any other applicable United States state securities laws.

General Information Only

This material is for general information only and is not an offer for the purchase or sale of any financial product or service. The material has been prepared for investors who qualify as wholesale clients under sections 761G of the Corporations Act or to any other person who is not required to be given a regulated disclosure document under the Corporations Act. The material is not intended to provide you with financial or tax advice and does not take into account your objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by Sandford Capital, Waterhouse VC or any other person. To the maximum extent possible, Sandford Capital, Waterhouse VC or any other person do not accept any liability for any statement in this material.

Financial Regulatory Oversight and Administration

Waterhouse VC is an Australian Unit Trust denominated in AUD and available to wholesale institutional investors worldwide with a minimum of AUD 500,000 or USD / EUR / GBP / JPY / CHF equivalent. This material has been prepared by Waterhouse VC Pty Ltd (ABN 48 635 494 861) (‘Waterhouse VC’, ‘Trustee’, ‘us’ or ‘we’) as the Trustee of the Waterhouse VC Fund (the ‘Fund’). The Trustee is a corporate authorised representative (CAR 1278656) of Sandford Capital Pty Limited (ABN 82 600 590 887) (AFSL 461981) (Sandford Capital) and appoints Sandford Capital as its AFS licensed intermediary under s911A(2)(b) of the Corporations Act 2001 (Cth) to arrange for the offer to issue, vary or dispose of units in the Fund.

Performance

Past performance of Waterhouse VC is not a reliable indicator of future performance. We make every endeavour to ensure results are accurate. Waterhouse VC Pty Ltd does not guarantee the performance of any strategy or the return of an investor’s capital or any specific rate of return. No allowance has been made for taxation, where applicable. We encourage you to think of investing as a long-term pursuit. Waterhouse VC’s results are indicative only and subject to subsequent year end external financial review.

Copyright

Copyright © Waterhouse VC Pty Ltd ACN 635 494 861. No part of this message, or its content, may be reproduced in any form without the prior consent of Waterhouse VC.

Governing Law

These Terms and Conditions of use are governed by and are to be construed in accordance with the laws of New South Wales. By accepting these Terms and Conditions of use, you agree to the non-exclusive jurisdiction of the courts of New South Wales, Australia in respect of any proceedings concerning these Terms and Conditions of use.