Waterhouse VC invests globally in publicly listed and private companies across the wagering and gaming ecosystem. The Fund is available to wholesale investors only.

Since inception (August 2019), Waterhouse VC has achieved a gross total return of +3,785% (72% p.a. annualised) as at 31 May 2026, assuming reinvestment of all distributions.

Nothing beats interaction

Barry Diller made his money betting on the future of media and technology. He greenlit blockbusters at Paramount, launched a TV network at Fox, and turned IAC into an internet giant.

Now, at 84, he is betting big on casinos.

People Inc., formerly IAC, has proposed buying the majority of MGM Resorts it does not already own, valuing the group at more than $18 billion. Days earlier, hospitality tycoon Tilman Fertitta agreed to buy Caesars Entertainment in a deal valuing the company at $17.6 billion.

Neither deal is final, but the timing is interesting. Capital is pouring into artificial intelligence, making gambling products quicker to build, easier to personalise and faster to scale. Land-based casinos are often treated as legacy assets.

Diller sees something different. MGM fits his definition of a real-world asset that AI “cannot easily replicate or disintermediate.”

Gambling is not governed by consumer preference alone. Regulation decides where activity can happen, which products exist and how much friction sits between the customer and the bet.

Land-based casinos still own something valuable: permission, place and people.

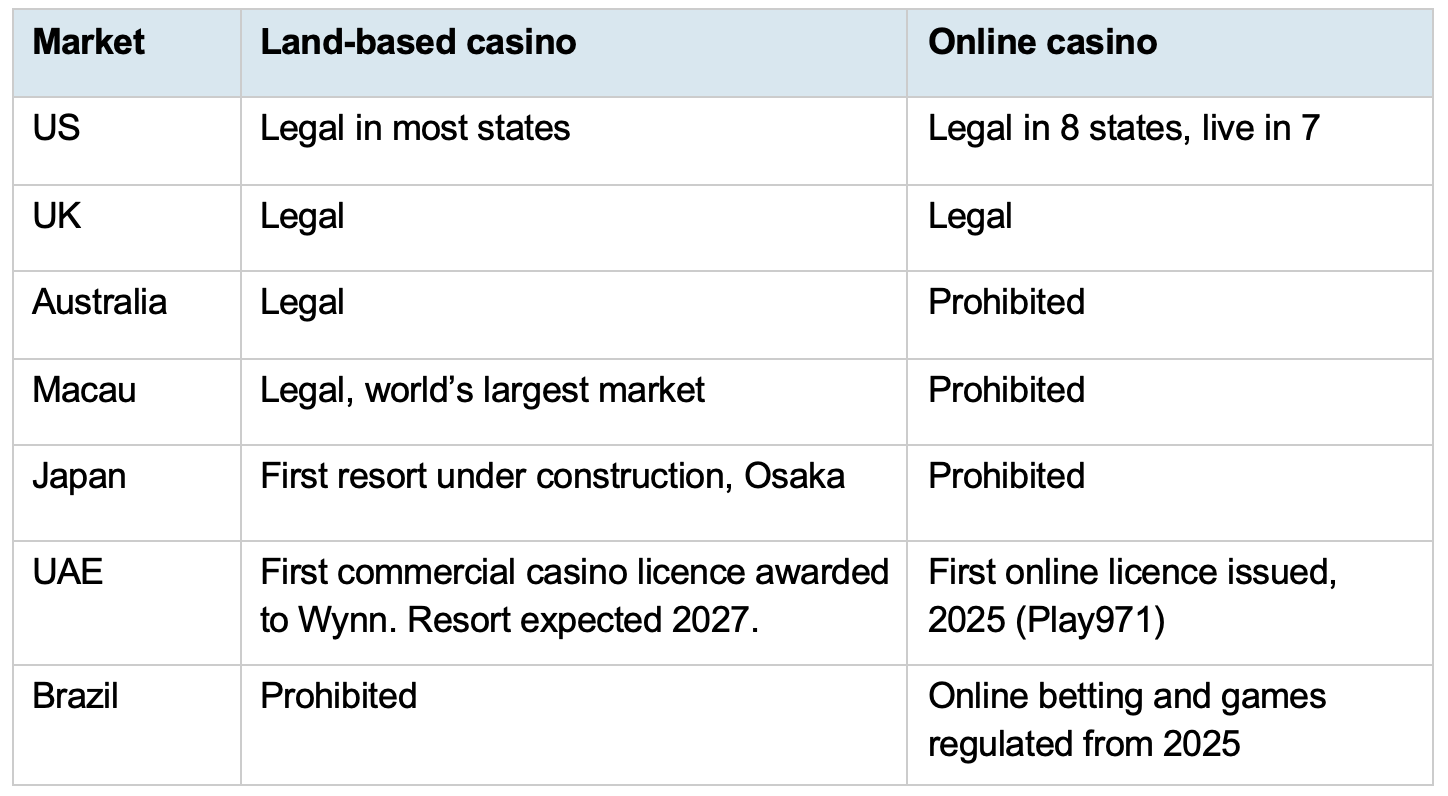

MGM’s Osaka integrated resort, due around 2030, and the emergence of licensed integrated resorts in the UAE show the same pattern. Governments are using scarce physical gaming licences to anchor tourism, hospitality and entertainment.

Online was meant to kill the betting shop. Exchanges were meant to kill the bookmaker. Crypto casinos, sweepstakes operators and prediction markets have all shown that when regulated markets leave gaps, demand finds another route.

Channels rarely disappear. When one is constrained, demand moves to whoever offers the best mix of access, experience and permission.

Land-based casinos still hold that mix. Permission, place and people are hard to replicate online. What they lack is the speed and interactivity of online. Closing that gap is the opportunity, and for Waterhouse VC the question is who captures it.

Speed and Access

For most of casino history, the venue was the distribution layer. The licence, the building and the geography controlled access.

An online operator can reach anyone with a smartphone, see how they play, personalise offers, cross-sell products and re-engage them in real time. Content moves at the same speed. An online studio can build a game in weeks and distribute it to hundreds of operators overnight. For example, SPRIBE's Aviator game reportedly processes hundreds of thousands of bets per minute.

An AI-generated live dealer from Octane Studios. Online products can test and iterate quickly. The physical floor moves far slower. Source: Octane Studios

European online gambling revenue reached €47.9 billion in 2024, and, on EGBA estimates, accounted for 39% of total gambling revenue. Casino is the largest online vertical at €21.5 billion, two and a half times its land-based equivalent. US iGaming grew 27.6% in 2025 to $10.74 billion, against 2.3% for traditional casino gaming.

An online sportsbook shows form, prices, live pictures, props and markets that never stop moving. An online casino shows jackpots, game history, recommendations, tournaments, streams and social proof. The operator can change the experience while the customer is still playing.

That is the standard land-based casinos now compete against.

Permission, Place and People

The case for land-based starts with permission. Online casino exists only where governments allow it. New Jersey launched in November 2013. More than a decade later, only eight US states have legalised it and seven are live. The rest stay closed, held back by tax, tribal interests and incumbent lobbying.

The seven live states generated more than $10 billion in 2025. In Pennsylvania and New Jersey online overtook commercial land-based revenue for the first time.

Scarcity creates value for those with permission, and it explains why leakage persists. The AGA estimates illegal and unregulated US gambling generates $53.9 billion a year and costs states $15.3 billion in taxes. Once a channel grows large and politically uncomfortable enough, pressure builds to bring it inside the regulated perimeter.

The second asset is place. A licence does not just grant permission. It fixes the business to a location: physical, visible, taxable, inspected and locally embedded. A casino employs local people and draws tourists. In Japan and the UAE, new licences are tied to building resorts that bring in visitors, not just approving a room full of machines.

The third asset is people, and place is what gathers them. A busy floor has hosts, regulars, groups, tourists, noise and the buzz of winning in front of others. That is part of what the customer pays for. It is the one thing a screen at home cannot reproduce.

Inside the Machine

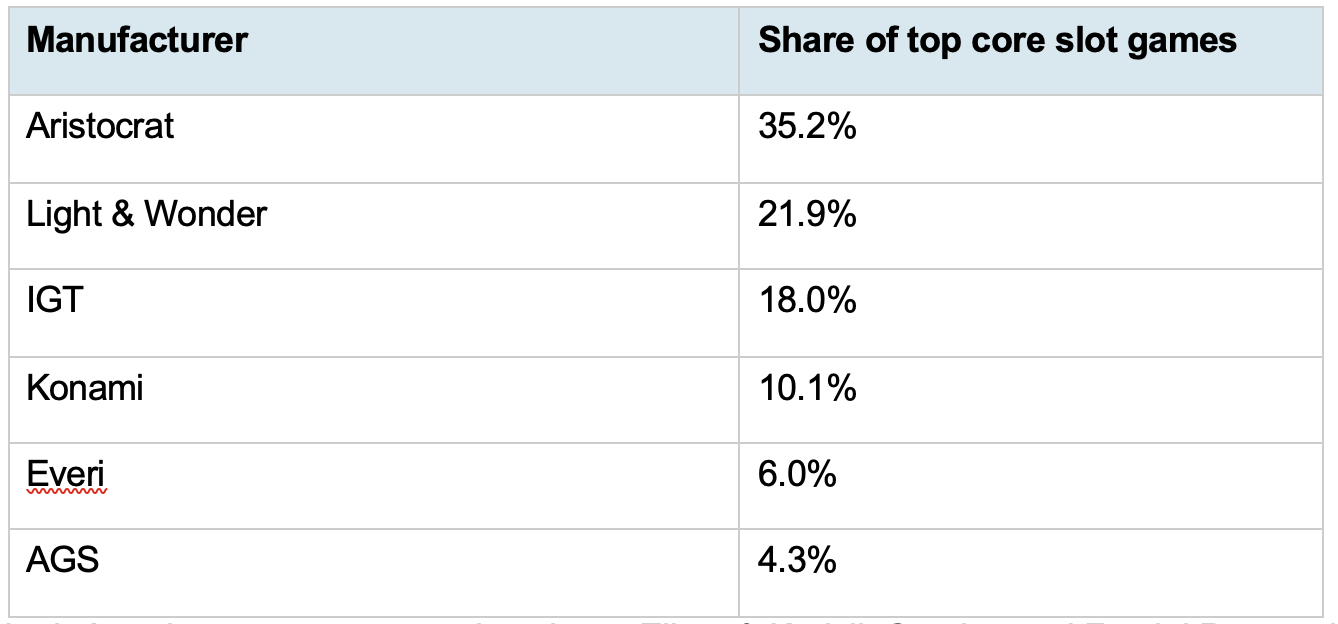

Across much of the market, innovation still starts and ends with the machine. The great destination resorts are the exception, where the whole property is the product. That reliance on the machine matters, because a handful of manufacturers control it.

North American core game market share, Eilers & Krejcik Gaming and Fantini Research, November 2023. IGT’s gaming division and Everi have since combined under Apollo.

That concentration has produced innovation in cabinet design, game maths, graphics, content and performance. But the wider floor experience has not moved with it.

The reason is structural. Manufacturers profit by making their own machines more valuable. They are hardware-led businesses. DoubleDown is a useful example. It launched the largest casino on Facebook in 2010, and IGT, then the biggest name in slots, bought it two years later for roughly $500 million rather than build its own.

A casino floor is different. It is not one manufacturer's showroom but a mixed environment, with cabinets, systems and data spread across several vendors. That makes floor-wide innovation difficult.

The manufacturers' incentives are machine-level. The operators' capabilities are venue-level.

Operators own the customer relationship and would benefit from a more dynamic floor, but their strengths are property, compliance, hospitality, loyalty and operations. They are not usually software companies.

As a result, the floor still relies on familiar tools: VIP hosts, loyalty cards, free play, mailers, drawings and slot tournaments on isolated banks of machines.

Operators know the online threat. MGM, Caesars, Penn and Boyd all run online casinos, and in Pennsylvania alone 24 licensed online platforms operate through land-based licence holders. In states where iGaming remains illegal, some operators have pushed into white-label social casinos instead.

But both of these follow the customer out of the building, into online channels where the venue has less control and keeps less of each dollar. They chase the customer onto the screen instead of making the floor itself better.

The bigger opportunity is the other way round: technology that brings players through the door and makes the floor feel alive once they are there.

The Opportunity

The machines themselves do not need to change. A slot machine is still a slot machine, and a table game is still a table game. The opportunity is everything around them: information, competition, rewards, social play and live events.

Every sportsbook lets a punter check form, prices and markets before committing. A customer on a casino floor walks past hundreds of machines with little sense of which to play or what is happening around them.

It could look like a Monday night video poker challenge. A floor-wide competition during March Madness. A live leaderboard among friends. A host pulling players into a timed tournament without shutting down a bank of machines. Rewards that respond to what is happening on the floor, not last month’s CRM cycle.

The machine stays physical. The layer around it becomes digital.

The scarce assets are already in place: the licence, the property, the machines and the customer standing on the floor. What is missing is the digital layer around it.

Waterhouse VC has taken an option in Slot Check, a business building into this layer. Slot Check surfaces machine-level performance information to players in near real time and supports challenges, tournaments and social play without altering licensed game hardware. The attraction is simple: it gives the physical floor some of the information, competition and engagement mechanics that online products already use.

Online casinos won on access and engagement, and the ease with which they can innovate. The floor owns what online cannot replicate: permission, place and people. The opportunity is not to make land-based casinos look like online casinos. It is to add a digital layer around the physical experience. That is where the supplier value sits, and where Waterhouse VC is focused: backing infrastructure that helps regulated operators compete.

Pitch Us

If you know any gambling tech companies seeking capital or distribution support, our 'Pitch' page makes it simple to connect with our investment team.

Media

Tom spoke to Ausbiz about how prediction markets platforms are seriously challenging the incumbent sportsbooks, the under-the-radar investor backing some of the world’s largest listed gambling companies.

For wholesale investors interested in following wagering and gaming industry news and trends, please follow our updates on Twitter (@waterhousevc) and WaterhouseVC.com.

All the best,

Tom

DISCLAIMER AND IMPORTANT NOTES

Performance shown is before all fees and expenses and assumes the reinvestment of all distributions on July 1. We make every endeavour to ensure results are accurate. The results are indicative only and subject to subsequent year end external financial review. Past performance is not a reliable indicator of future performance.

Please note the above information in relation to SPRIBE, MGM Resorts, IAC, Aristocrat, Light & Wonder, IGT, Konami, Everi, AGS, Apollo, Caesars Entertainment, Penn Entertainment, Boyd Gaming, DoubleDown Interactive, Wynn Resorts and Slot Check is based on publicly available information and should not be considered nor construed as financial product advice. The Fund has taken an option in Slot Check. The information provided in this document is general information only and does not constitute investment or other advice. Readers should consult and rely on professional investment advice specific to their individual circumstances.

Not for Release or Distribution in the United States of America

This material may not be released or distributed in the United States. This material does not constitute an offer to sell, or a solicitation of an offer to buy, any securities in the United States or any other jurisdiction in which such an offer would be illegal. The units in the Fund have not been, and will not be, registered under the U.S. Securities Act of 1933, as amended (the U.S. Securities Act) or the securities laws of any state or other jurisdiction of the United States. Accordingly, the units in the Fund may not be offered or sold in the United States unless they are offered and sold, directly or indirectly, in transactions exempt from, or not subject to, the registration requirements of the U.S. Securities Act and any other applicable United States state securities laws.

General Information Only

This material is for general information only and is not an offer for the purchase or sale of any financial product or service. The material has been prepared for investors who qualify as wholesale clients under sections 761G of the Corporations Act or to any other person who is not required to be given a regulated disclosure document under the Corporations Act. The material is not intended to provide you with financial or tax advice and does not take into account your objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by Sandford Capital, Waterhouse VC or any other person. To the maximum extent possible, Sandford Capital, Waterhouse VC or any other person do not accept any liability for any statement in this material.

Financial Regulatory Oversight and Administration

Waterhouse VC is an Australian Unit Trust denominated in AUD and available to wholesale institutional investors worldwide with a minimum of AUD 500,000 or USD / EUR / GBP / JPY / CHF equivalent. This material has been prepared by Waterhouse VC Pty Ltd (ABN 48 635 494 861) (‘Waterhouse VC’, ‘Trustee’, ‘us’ or ‘we’) as the Trustee of the Waterhouse VC Fund (the ‘Fund’). The Trustee is a corporate authorised representative (CAR 1278656) of Sandford Capital Pty Limited (ABN 82 600 590 887) (AFSL 461981) (Sandford Capital) and appoints Sandford Capital as its AFS licensed intermediary under s911A(2)(b) of the Corporations Act 2001 (Cth) to arrange for the offer to issue, vary or dispose of units in the Fund.

Performance

Past performance of Waterhouse VC is not a reliable indicator of future performance. We make every endeavour to ensure results are accurate. Waterhouse VC Pty Ltd does not guarantee the performance of any strategy or the return of an investor’s capital or any specific rate of return. No allowance has been made for taxation, where applicable. We encourage you to think of investing as a long-term pursuit. Waterhouse VC’s results are indicative only and subject to subsequent year end external financial review.

Copyright

Copyright © Waterhouse VC Pty Ltd ACN 635 494 861. No part of this message, or its content, may be reproduced in any form without the prior consent of Waterhouse VC.

Governing Law

These Terms and Conditions of use are governed by and are to be construed in accordance with the laws of New South Wales. By accepting these Terms and Conditions of use, you agree to the non-exclusive jurisdiction of the courts of New South Wales, Australia in respect of any proceedings concerning these Terms and Conditions of use.