Welcome to the January 2021 newsletter for the Waterhouse VC Fund.

The Fund specialises in gambling assets and businesses that are related to the gambling industry. The industry is under-researched by most mainstream fund managers. We aim to leverage our unique expertise and existing assets to generate capital growth for investors over the long-term.

Since inception in August 2019, the Waterhouse VC Fund has achieved a total return of 1,025% ($11.25 unit price), as at 31 December 2020.

The land grab in the land of opportunity

In 1895, Charles Edgar Duryea founded Duryea, America’s first car company. Subsequent technological developments and the insatiable demand for cars led to a rush of automobile entrepreneurs. Over the ensuing decades, more than 1,900 car companies were formed by new startups and ‘old world’ companies entering car production. The economic turmoil of WWI and the Great Depression contributed to a reduction in the number of automakers and by the 1950s the remaining companies in the U.S. were squeezed out by competition or merged with larger companies to form the “Big Three” (Chrysler, Ford and General Motors).

A driver of automaker consolidation was the scale required for the mass production of cars. Larger investments in production lines reduce the average cost of a car, a key advantage to bigger companies in a low-margin industry. M&A deals can also expand geographical coverage and drive scale benefits in marketing. By 2017, just five companies produced 43% of the world’s vehicles. The industry has come a long way since Duryea.

You can probably see where we’re going with this. The history of the U.S. auto industry provides a great analogy for the current online gambling boom. As we wrote in our September 2020 update, the industry is in a highly competitive phase with new startups every month, entrants from overseas, and competition from the ‘old guard’ of land-based casinos. But we don’t believe it will look that way in the long-term.

We’ve seen a rush to launch, invest, partner and acquire - typical of a booming industry. Most recently, we’ve seen hotel and casino group MGM Resorts International make an offer (which was subsequently withdrawn) for the U.K.’s Entain (formerly known as GVC Holdings), MGM’s JV partner in the States and owner of brands like Ladbrokes. The acquisition would have provided strategic certainty by giving MGM full control of its sports betting and igaming tech stack, which is a similar rationale to the recent Caesars-William Hill and DraftKings-SBTech mergers. The tech stack is the ‘production line’ of online gambling, and the foundation for providing a superior customer experience. A unified tech stack provides cost savings compared to running multiple systems in parallel.

MGM management may also have seen economies of scale in bringing the two U.S. businesses closer together. The JV business, BetMGM, now has 18% market share across all live states. The MGM casino business has mass market reach while online is the superior channel for sports betting. Cross-selling a casino database to online sports betting could create a more integrated experience and quickly expand geographical reach. Just like with autos, only mega brands can afford the prized national media, like sponsoring the NBA or NFL, driving lower customer acquisition costs.

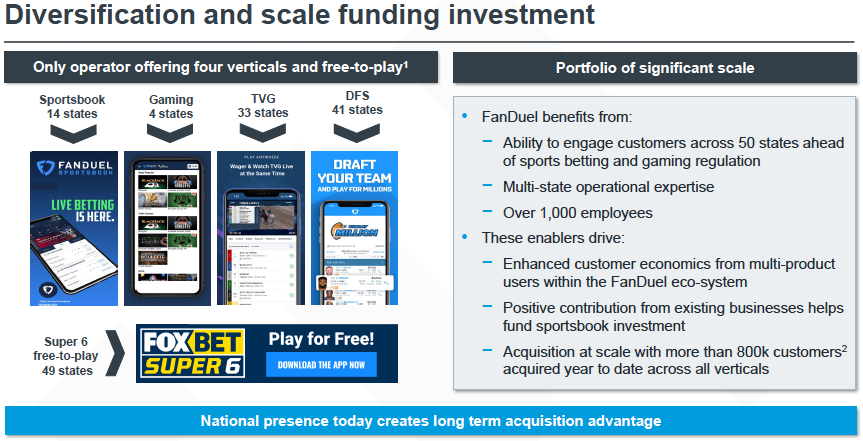

In a similar vein, last month Flutter Entertainment announced that it is securing control of its U.S. business by increasing its stake in America’s leading fantasy sports and sports betting business FanDuel from 57.8% to 95%. FanDuel has more than 8.5m customers across America, anchored by its core fantasy sports customer base that was built up over many years before gambling was legalised. The company has around 50% market share in New Jersey, the country’s largest online sports betting market with around 20 competitors.

EGM Investor Presentation, for acquisition of 37.2% of FanDuel, 29 December 2020

FanDuel’s sellers will receive US$4.18bn in cash and shares for the 37.2% stake, which values the total business at an enterprise value of US$11.2bn. FanDuel’s revenue run-rate of US$860m indicates a valuation of 13X forward EV/Revenue, significantly less than the DraftKings (FanDuel’s closest comparable) 33X forward EV/Revenue multiple (US$18bn enterprise value, US$550m revenue). Businesses growing market share within a multi-year growth industry are very difficult to find and even harder to buy for an attractive price. Illustrating the benefits of scale, DraftKings co-founder, Paul Liberman, said, “A large part of why FanDuel and DraftKings are doing so well in this market is that established customer base”.

Flutter’s 95% stake will contribute circa US$817m to group revenue (around 11.7% of total revenue). Flutter is funding the purchase through a share issue (US$2.16bn), available cash (US$0.54bn) and a placement (US$1.48bn). Post-acquisition, management expects net debt/EBITDA of circa 3X, above their 1-2X long-term target. Flutter has stretched beyond their target leverage ratio before, with net debt/EBITDA of 3.5X after the merger with The Stars Group. Flutter should convert close to 25% of revenue to EBITDA this financial year and easily cover all interest obligations. Flutter is a highly cash generative and well-run group, so we anticipate it should not have any issues supporting this debt.

The U.S. market is still maturing and the availability of legal online sports betting and land-based sportsbooks is increasing state-by-state. It will be some time before we see the level of consolidation of mature betting markets like the U.K. and Australia, where the top three mega brands have over 50% combined market share. In Italy, Europe’s second largest online gambling market, the six largest sites enjoy 70% market share of online sports betting. Similar to the past consolidation of the global auto industry and mature betting markets in other countries, we envision a U.S. online betting market with a handful of firms earning the lion’s share of revenues and profits. We are confident that Flutter will be one of the handful.

For wholesale investors that want to follow gaming’s global growth, please follow us for updates on Twitter @waterhousevc.

Please note the above information in relation to MGM Resorts International, Entain, Flutter Entertainment and DraftKings is based on publicly available information in relation to each of them and should not be considered nor construed as financial product advice. The Fund currently has a position in Flutter Entertainment. The information provided in this document is general information only and does not constitute investment or other advice. Readers should consult and rely on professional investment advice specific to their individual circumstances.